Institutional darling Sam Bankman-Fried’s FTX has collapsed and vaporized at least $1 billion dollars of customer funds. Founder and CEO Sam Bankman-Fried (SBF) rapidly transformed from golden boy to town whipping boy. The collapse of FTX and its 130 affiliated companies has taken SBF’s net worth from a peak of $26 billion to virtually nothing. Echoing the fate of many of his customers.

What H.A.P.P.E.N.E.D? Sam may “not know” but it’s pretty obvious to everyone following closely. We’ll cover the events that led to the downfall of FTX and one of history’s greatest-ever destructions of wealth.

Seeds of Doubt – Nov 2nd

SBF’s cryptocurrency empire was officially divided into two main entities: FTX (his exchange) and Alameda Research (his trading firm). Both were giants in their respective industries. In theory, they were two separate businesses but doubt began to arise on November 2nd when a leaked balance sheet revealed that Alameda Research’s portfolio was full of FTX and FTT tokens.

This leak suggested that Alameda’s reserves were largely made up of a coin that its sister company minted (FTT/FTX), as opposed to an independent asset like a fiat currency or another crypto. The document reveals just how much of a giant Alameda was at its peak. The firm held assets totaling $14.6 billion dollars as of June 30th. Its single biggest allocation was $3.66 billion of “unlocked FTT”. The third largest entry on the assets side? 2.16 billion dollars worth of “FTT collateral”.

It was extremely risky for the majority of the net equity within Alameda to be FTX’s own centrally controlled and infinitely printable token. Alameda CEO Caroline Ellison declined to comment on the leaked balance sheet at the time; this only fed users’ growing doubt.

Wheels in Motion – Nov 5th – Nov 6th

If the balance sheet raised eyebrows, the events of the next couple of days raised alarms. Whale Alert notified its Twitter followers of just under 23 million FTT (valued at $584.5 million) transferring from an unknown wallet to Binance, the world’s largest centralized exchange. Commenters were quick to speculate that Binance’s CEO Changpeng Zhao (CZ) was behind the massive transfer.

The next day Caroline Ellison attempted to conduct some damage control and directly addressed the circulating balance sheet information. The Alameda CEO would claim that the leaked balance sheet was not reflective of the whole story and that over $10 billion dollars of assets were not disclosed in the documents.

Later that same day, CZ announced that Binance would liquidate its entire FTT holdings, citing “recent revelations that have come to light”. CZ would go on to say that Binance would conduct the massive sell-off in a way that minimizes market impact, claiming that the process would take a few months to complete.

Ellison was quick to respond to the announcement with a proposition. She suggested that Alameda would be happy to buy all of the FTT from Binance at a price of $22 (roughly market value at the time).

The Bank Run Begins – Nov 7th

With the very public airing of Alameda/FTX/Binance drama, FTX users begin withdrawing funds from the exchange at a rapid pace. Crypto Twitter was quick to suggest users get their funds out of FTX.

Reported data from Nansen on November 7th showed that stablecoin outflows on FTX reached $451 million over seven days, and users began to report sluggish withdrawals on FTX. The exchange addressed the withdrawal complaints by claiming everything was actually running smoothly. (Gaslighting?!)

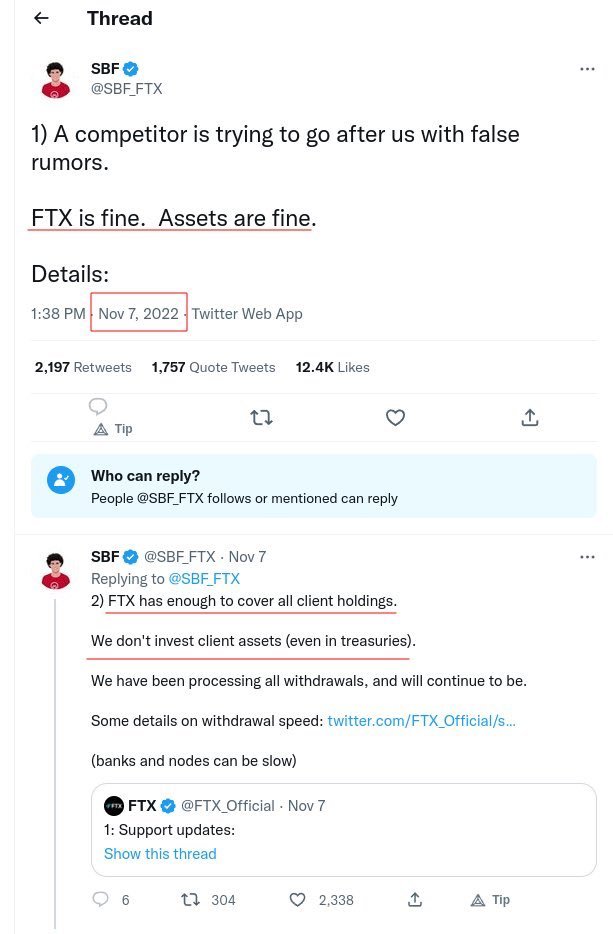

SBF fired off a series of tweets (now deleted) claiming that a competitor “is trying to go after us with false rumors” and added some assurances that “FTX is fine. Assets are fine”. The FTX CEO claimed that they held $1 billion in excess cash and called on CZ to “work together for the ecosystem”.

Responding to a question on Twitter, CZ signaled his disinterest in taking up the deal earlier poised by Ellison to buy Binance’s FTX Token holdings for $22 per token, saying, “I think we will stay in the free market”.

“An Agreement on a Strategic Transition” – Nov 8th

As the price of FTX began to waiver and the general crypto markets began to buckle under the suspense, SBF announced that FTX had “come to an agreement on a strategic transaction” with Binance for the exchange to help cover what he called a “liquidity crunch”.

SBF assures customers that “all assets will be covered 1:1”. CZ would go on to announce that Binance had signed a nonbinding letter of intent to acquire the exchange, but noted that it reserved the right to “pull out from the deal at any time”. SBF would go on to delete the Tweet that suggested a competitor was “going after us”, which also contained the now infamous “Assets are fine” comment.

Sea of Red – Nov 9th

It would take less than 48 hours for Binance to announce that they would not be pursuing the acquisition of FTX. The announcement cited that the alleged “mishandled customer funds and US agency investigations” led to the decision. The exchange would go on to add that “the issues are beyond our control or ability to help”.

The crypto market responded harshly as investors began to panic. Bitcoin’s price would hit a multiyear low of $15,600. SBF would go on to tell investors that he needed “emergency funding” to cover a shortfall of up to $8 billion dollars.

Foreshadowing the near future, the websites for FTX’s venture capital arm, FTX Ventures, and Alameda were taken offline on November 9th. Rumors would begin to circulate that FTX’s entire legal and compliance staff quit the day before.

After the website was brought back online, users were prompted with a warning strongly advising against depositing and stating that the exchange was unable to process withdrawals.

Too Little, Too Late – Nov 10th

SBF would finally buckle and release a statement apologizing for FTX’s insolvency. He would go on to blame “poor internal labeling of bank-related accounts” that led to him misunderstanding the severity of the company’s leveraged positions.

According to reports citing internal sources at Alameda, all employees at the trading firm quit collectively on November 11th after a group meeting. The reports of Alameda employees resigning came just a day after SBF said that the operations at Alameda Research would be shut down soon.

Chapter 11 – Nov 11th

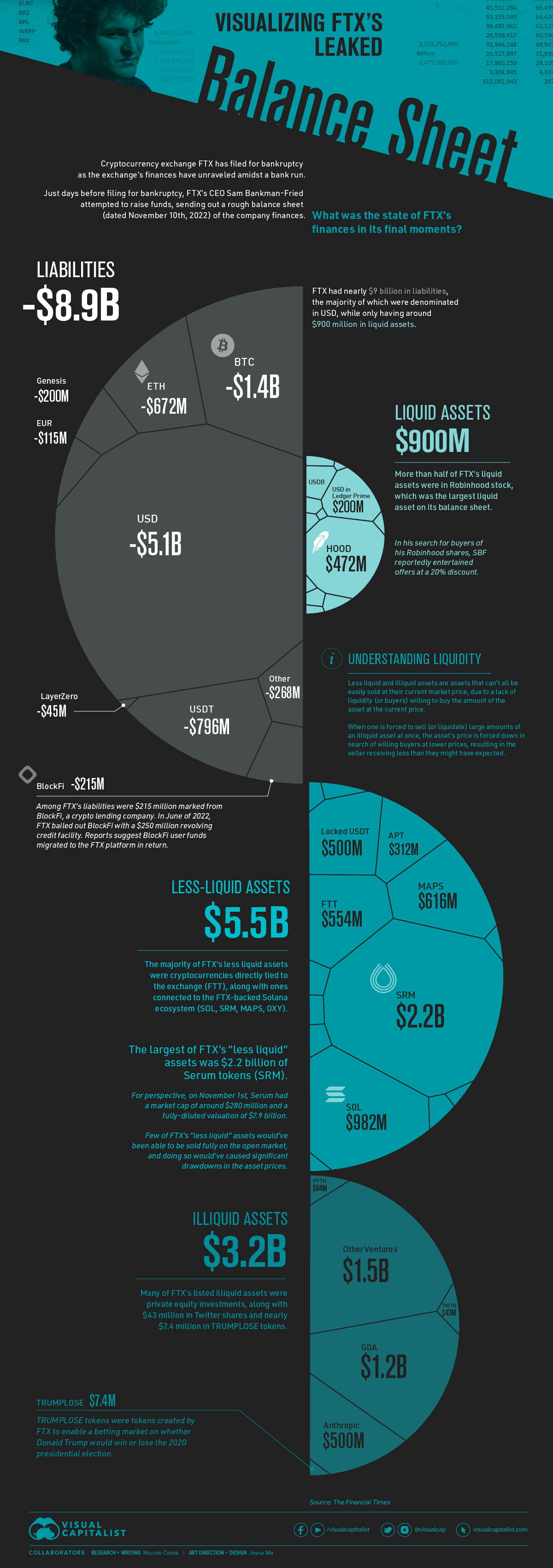

After several rumors about FTX facing an $8 billion hole on its balance sheet, Zane Tackett, the former head of the institutional arm at FTX, confirmed on Twitter that the exchange currently has liabilities worth $8.8 billion.

SBF would go on to announce that roughly 130 companies in FTX group had started proceedings to file for Chapter 11 bankruptcy in the US. SBF would step down from the CEO position and would be replaced by John Ray III, the lawyer behind the insolvency of energy giant Enron.

Conclusion

In less than a fortnight, SBF went from CEO of one of the largest centralized exchanges in the world to the face of the latest scandal to rock the financial sector. SBF and FTX are currently under investigation from the below agencies, with more sure to follow:

- The Financial Services Agency of Japan

- The Department of Financial Protection and Innovation in the State of California

- The Royal Bahamas Police Force

- Turkey’s Financial Crimes Investigation Agency

- The Manhatten District Attorney’s Office

Sam Bankman-Fried, along with FTX co-founder Gary Wang and director of engineering Nishad Singh, are understood to be in the Bahamas and “under supervision” by the local authorities, according to a source familiar with the matter.

The full ramifications of this event are still yet to unfold as more and more crypto projects reveal their exposure to FTX’s collapse. The downfall of this crypto empire has ushered in the latest iteration of crypto winter as the community braces for the chilling aftermath of this saga.

{kind=link}