Under SBF’s “control,” it appears as though FTX had little to no idea of how much cash was on hand at any moment or where the cash was being held.

After FTX and FTX US filed for chapter 11 bankruptcy, there were a lot of rumors floating around about how the exchange giant managed to get itself into such a massive hole. Many wondered how a corporation of this size managed to fail so spectacularly, and allegations of misappropriated funds spread like wildfire.

The bankruptcy filings have now been made public, and suspicions of nefarious activities have been validated. It turns out that FTX was one of the most poorly run operations in recent history, especially when considering the exchange’s size and influence. The records of an institution once valued at $32B look more like the remnants of a failed college start-up than a globally influential crypto exchange.

The new CEO of FTX, John J. Ray III, was appointed on Nov. 11 to oversee the bankruptcy filings and restructuring of FTX post-collapse. Mr. Ray III has over 40 years of legal and corporate restructuring experience, most notably supervising Enron’s unwinding after fraudulent malfeasance from executives. The statement made by Mr. Ray III in the FTX filings confirmed the rumors of complete incompetency on the part of FTX executives; he said:

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here.”

Damaging Discoveries

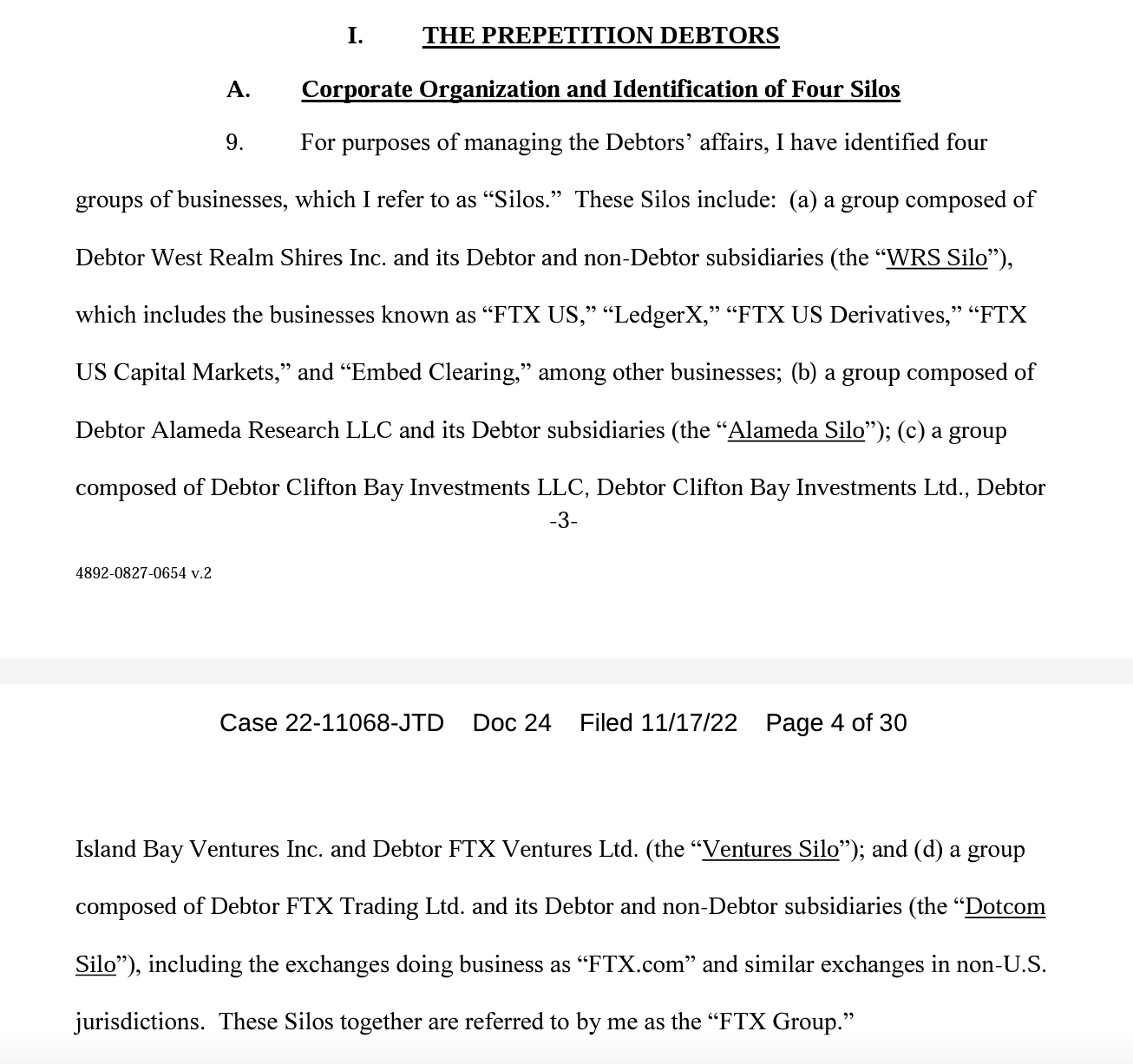

The bankruptcy filing separates FTX into four ‘Silos.’ Each silo is a group of businesses operating under the FTX entity controlled by Sam Bankman-Fried and co.

Mr. Ray III stated in the filings that he “did not have confidence” in the quarterly financial reports generated for each silo under SBF’s control, as the reports were unaudited and “the information may not be correct as of the date stated.”

This remark appears for each of the silo reports…

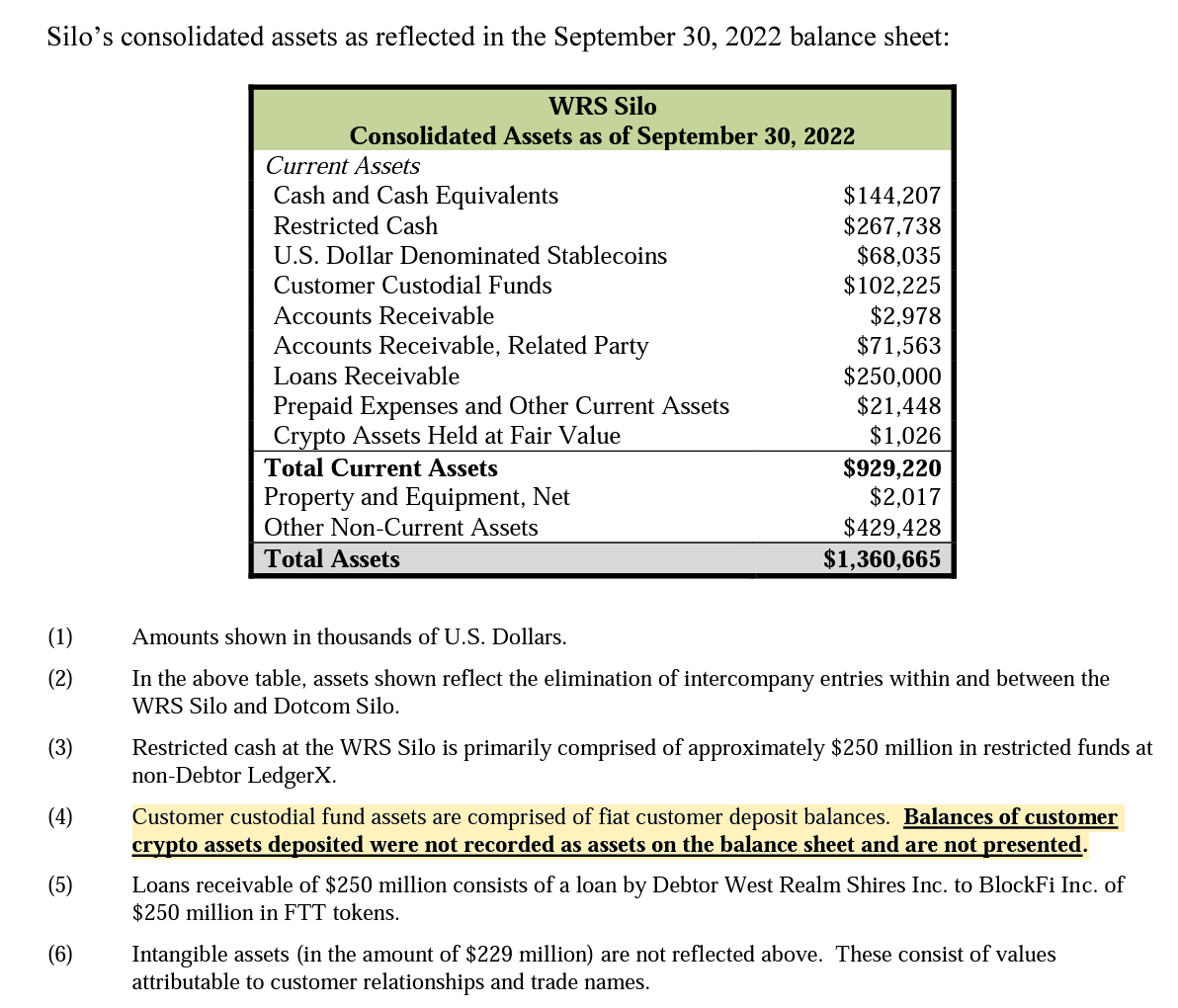

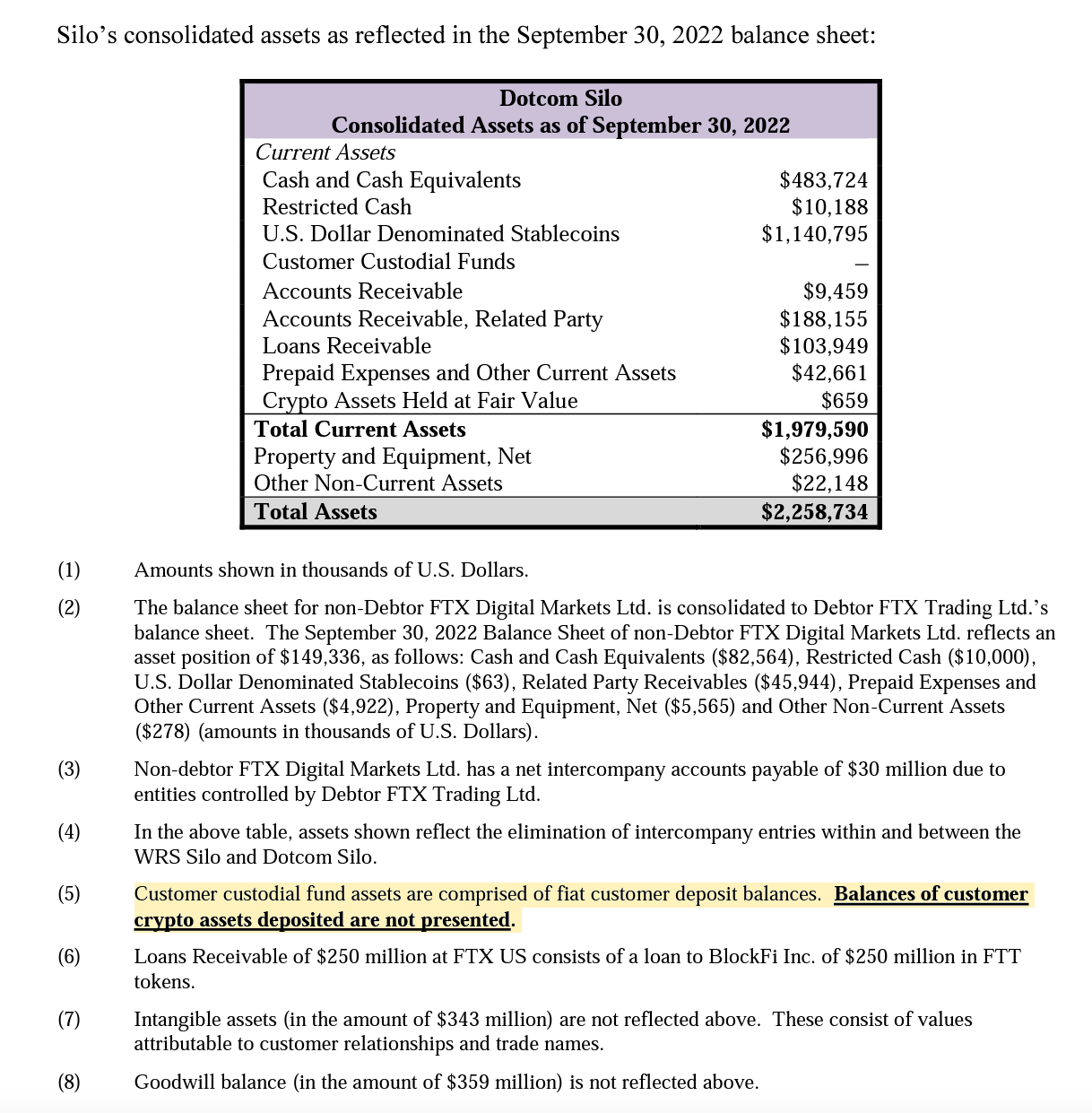

The financial reports themselves are alarmingly nonspecific. A glaring example is the absence of customer crypto asset records; it seems they were thrown in a general account for whatever use.

Some examples of financial reports as of Sept. 2022:

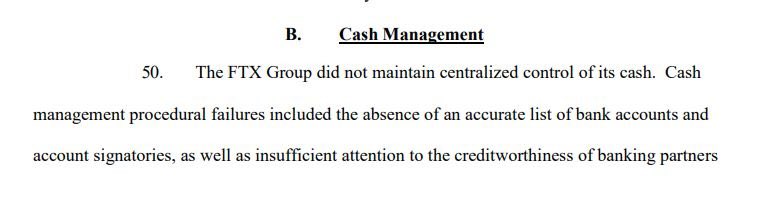

Effective cash management was almost non-existent. Under SBF’s “control,” it appears as though FTX had little to no idea of how much cash was on hand at any moment or where the cash was being held.

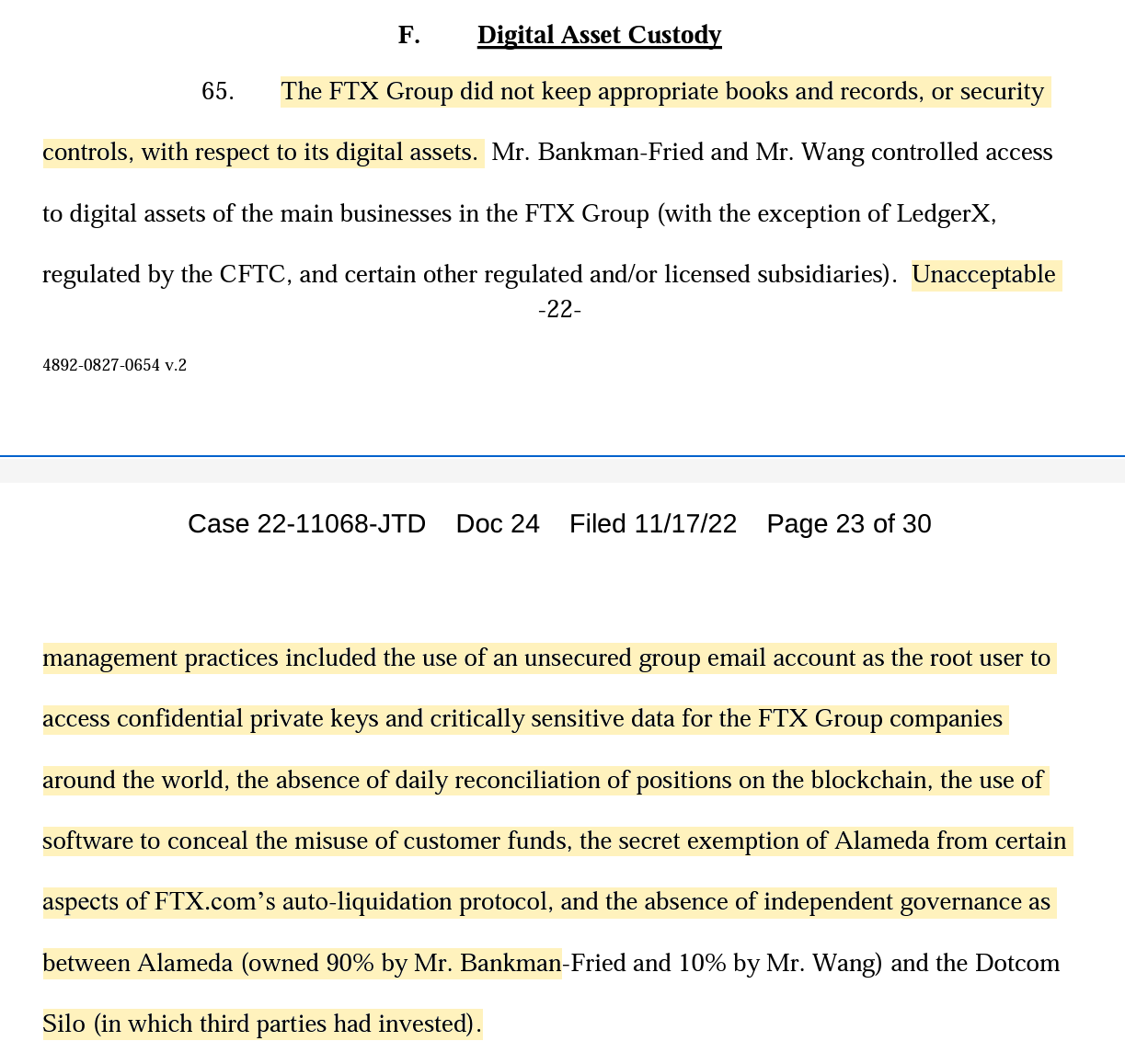

Record keeping and management, and security practices were just as appalling. The filings show that critically sensitive information was shared via unsecured email groups, software being used to conceal the misuse of funds, and the “secret exemption of Alameda from certain aspects of FTX’s liquidation pool.”

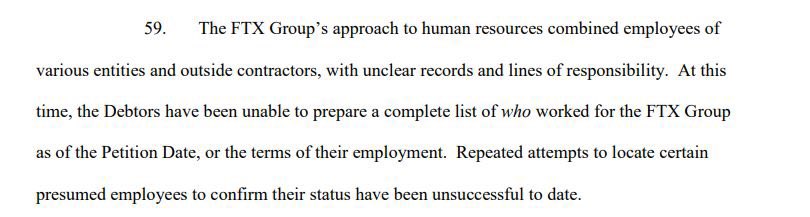

Continuing the theme of horrendously bad (perhaps intentionally bad?) record keeping, it appears that several employees could not be located or accounted for by the debtors now in possession of FTX.

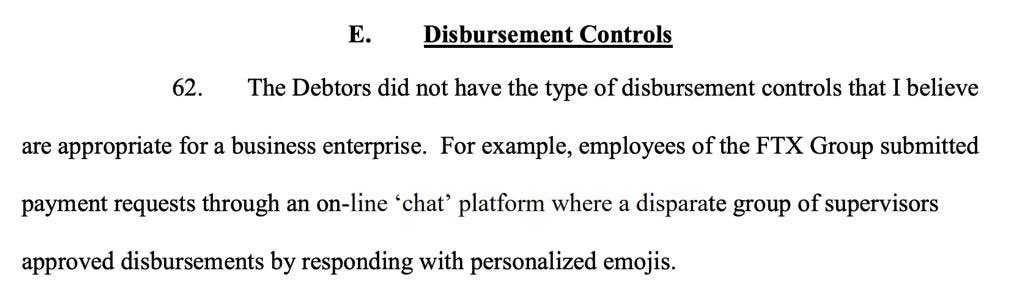

Employee loans and expense reimbursements were also, to little surprise, extremely dodgy and dysfunctional. Expense reimbursement requests were accepted or denied using, wait for it, EMOJI REACTIONS from some manager in charge.

Executives were also given huge loans from Alameda Research for who knows what. Rest assured, these loans were approved with the appropriate emoji.

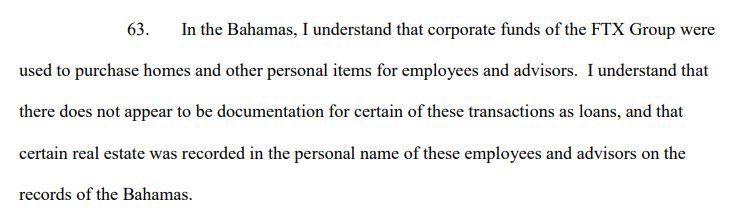

Maybe these loans were used to purchase real estate, as it appears company funds were used to buy property under the names of employees…

Thoughts…

The evidence of complete mismanagement of FTX, either due to complacent misconduct or utter ignorance, is staggering. How an institution like FTX could dominate the industry for any length of time is beyond me. This entire case reeks of fraudulent and malicious behavior by all parties involved, and the complete lack of internal self-regulation and external corporate due diligence boggles the mind.

How can we continue to trust those in positions of power? We can’t.

Trustlessness > trust.