Welcome friends!

Are you tired of doing research? Are there more important things in your life than combing through DeFi documentation in hopes of understanding what the hell is going on? If you answered yes to either of these questions you’ve come to the right place. Today I will be providing a brief overview on everything you need to know about the 0VIX Protocol, a recently launched Polygon-native DeFi money market.

To preface the overview, let’s review some money market basics…

What are DeFi Money Markets?

Money markets are where users go to lend and/or borrow assets. Lending and borrowing in DeFi can be confusing; most money markets in DeFi require over-collateralization – supplying more capital in order to borrow less. I often get asked about the use-cases of over-collateralized loans; “why would I deposit $100 just to borrow $70? Why not keep the $100?” The reason is because oftentimes you are supplying an asset that you wish to continue holding. Maybe you have come across some unexpected expenses that you need cash to pay for, but all the crypto assets you own are not ones you wish to sell because “they’re all going to the moon!” Money markets enable you to borrow capital against your assets without having to sell them. Or maybe you don’t need cash right now but you wish to get some yield on your crypto; lending markets are a place to park your assets in return for interest paid to you by the borrowers.

Health Factor, LTV Ratio and Utilization Rate

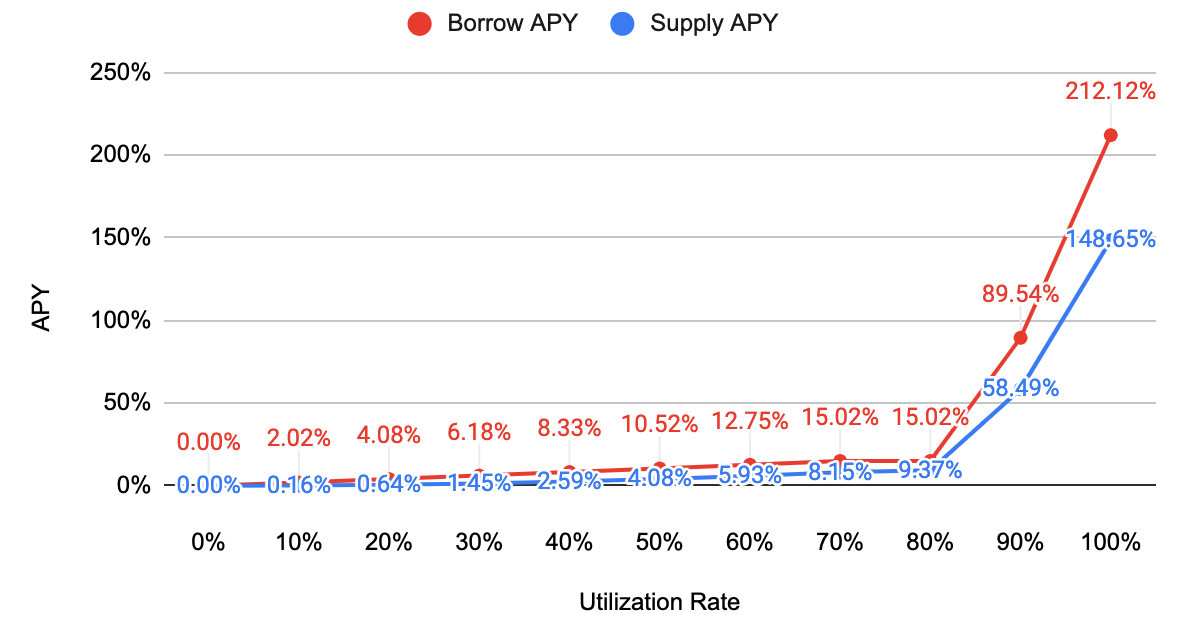

Interest rates in DeFi lending markets are set algorithmically, based on the supply and demand in a particular market. The biggest factor that influences supply and borrow rates is the utilization rate. Utilization measures how much of a market has been loaned out to borrowers; for example, if I have a market consisting of $100 USDC and $80 USDC has been loaned out, the utilization rate in this market is 80%. If utilization reaches 100%, that is if the entire market has been loaned out, suppliers will be unable to withdraw their funds until some loans have been repaid.

A health factor measures the health of a position. The higher your health factor, the less of a chance there is of liquidation – losing your supplied/deposited assets. If your health factor drops below 1, some of your supplied assets will be liquidated due to the value of their collateral not covering the value of their borrowed assets. A health factor depends on the LTV ratios of the assets in question.

LTV stands for “loan-to-value”. It determines the maximum amount a user can borrow based on their collateral. For example, if ETH has an LTV Ratio of 70%, for every $1 of ETH deposited, $0.70 worth of assets can be borrowed.

0VIX Protocol

0VIX is a native to the Ethereum L2 Polygon. 0VIX launched in March of 2022, founded by the team behind GOGO Protocol. The 0VIX mission is to provide straightforward, permissionless lending and borrowing while offering competitive rates to their users. They are also the first lending market to implement a veTokenomics design model (more below!).

The money market scene in DeFi is a tough industry to find room in. The top two lending markets in the space currently host over 15% of the total value locked in all of DeFi. This concentration can make it hard for new lending markets to gain market share, especially in a bear market. 0VIX is aware of this, and they have come up with their own solutions to capture new users and make them stick.

Interest Rate Model Advancement

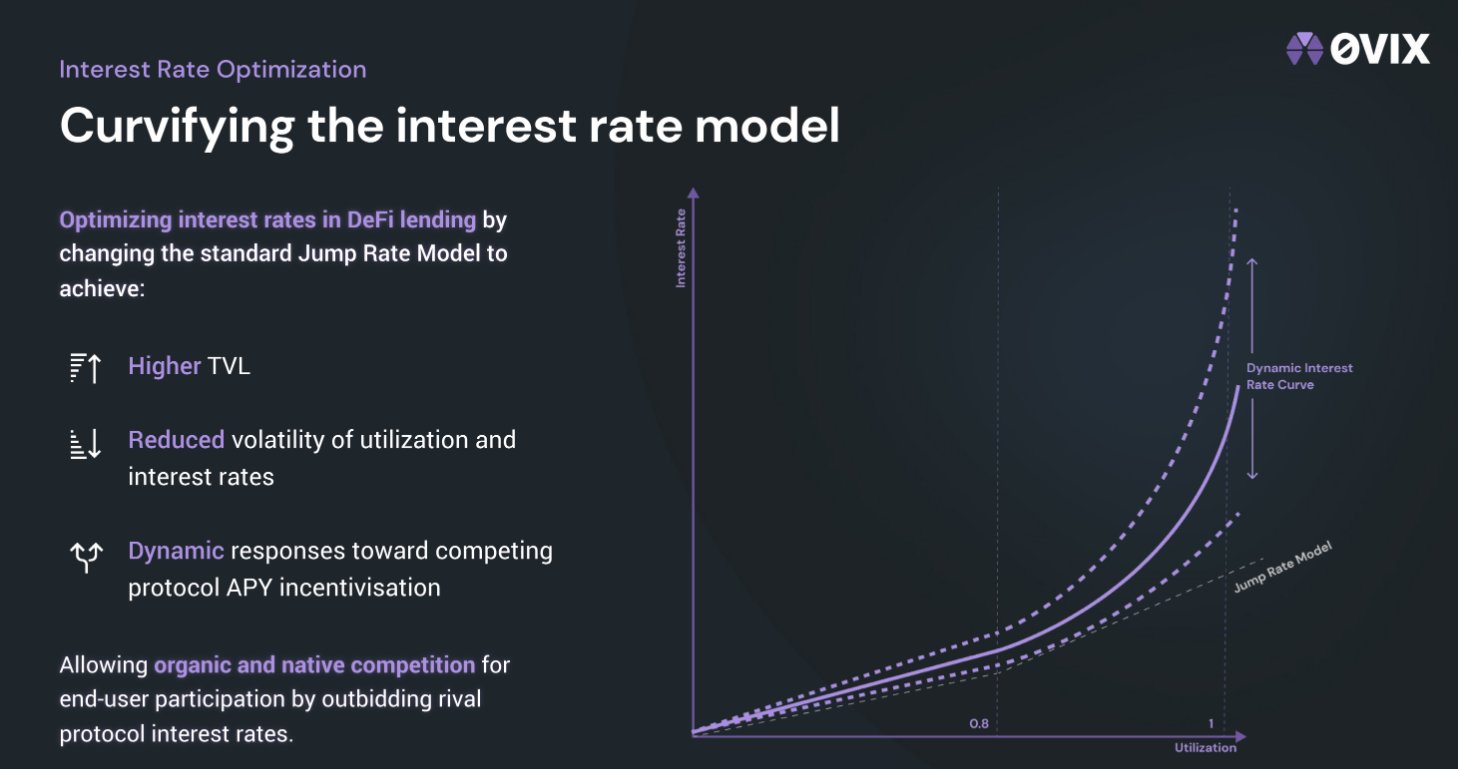

The “kinked” interest model, also known as the Jump Rate interest model, has been the standard in DeFi lending markets over the last couple years. In this model, interest rate adjustments depend largely on market utilization rate threshold; once that threshold is reached within a market, interest rates will dramatically increase for both suppliers and borrowers. This incentivizes borrowers to pay back their loans and suppliers to deposit more.

Kinked/Jump Rate Model

0VIX has advanced this model by developing a dynamic interest rate model, designed to smooth the increase of rates as utilization increases, and to reduce the volatility of both interest and utilization rates. This model aims to solve an interest rate arbitrage problem that occurs between different lending protocols. If the USDC supply rate on lending platform #1 is higher than the USDC borrow rate on lending platform #2, market participants will take advantage of the difference and drain USDC liquidity from #2 to deposit into #1. The model 0VIX has deployed responds dynamically to competing interest rates across other lending markets in order to reduce the risk of liquidity extraction.

0VIX Dynamic Interest Rate Model

oTokens

0VIX has taken a page out of Compound’s interest-bearing token (ibToken) model when it comes to interest earned on assets supplied. When a user deposits an asset (e.g. USDC) on 0VIX, they receive an oToken in return (oUSDC). These oTokens are interest-bearing, meaning they are continually increasing in value relative to their underlying versions. By holding oTokens in a wallet, users are earning interest on their supplied asset. Whenever a user wishes to redeem their deposit, they need only return the oTokens in exchange for the asset supplied plus interest accrued.

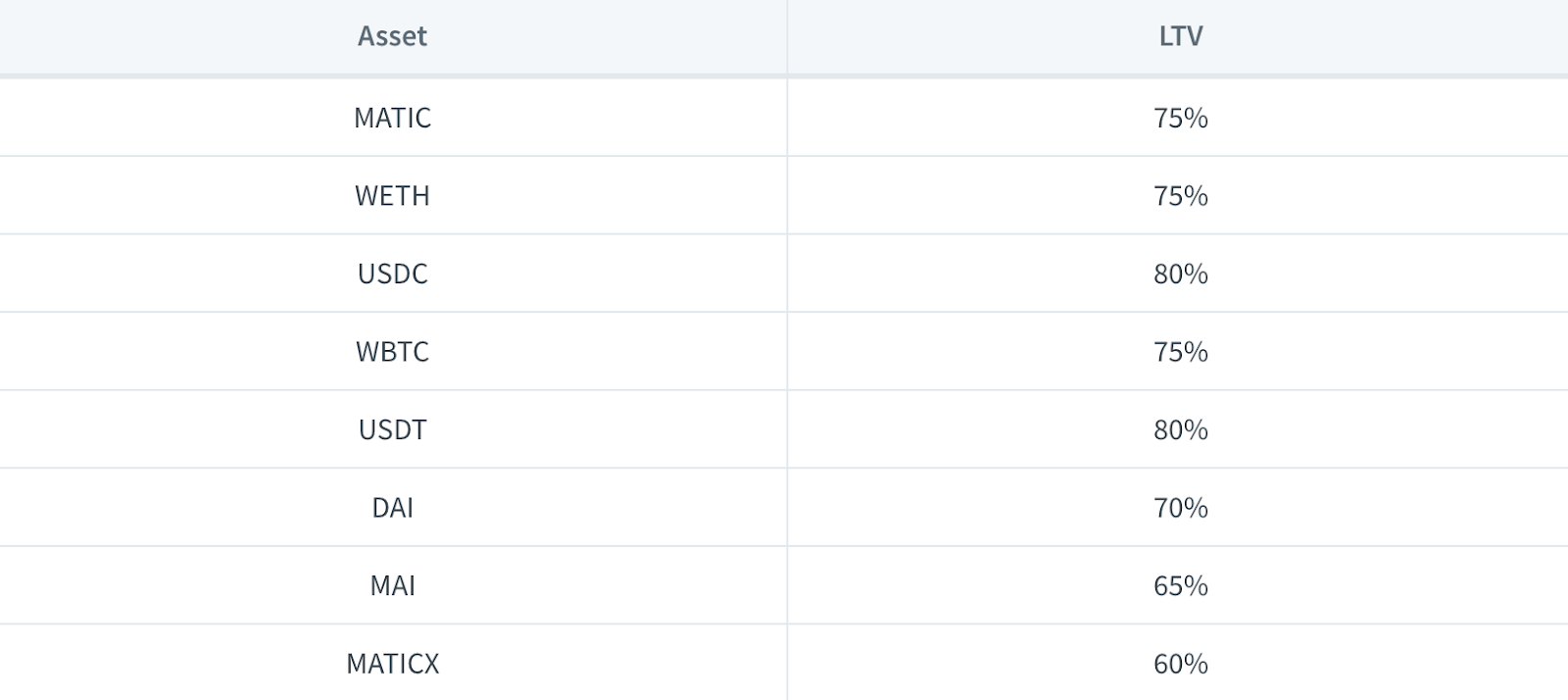

Supported Tokens and Respective LTV Ratios

The table below displays all assets supported by 0VIX and their respective LTV ratios. These assets are available to be lent or borrowed.

The $VIX Token

$VIX is 0VIX Protocol’s native token. $VIX is not currently available for trade yet, as the token is still currently being distributed to the community via “pre-mining” incentives. At time of writing, users who deposit and/or borrow on 0VIX will be rewarded with a portion of the initial supply of $VIX. The rewards program runs in 1-week epochs at random times – each week borrowers and suppliers are rewarded with an amount of $VIX proportional to the amount supplied or borrowed.

The reward rates vary depending on the asset(s) supplied/borrowed and can be found on the application’s homepage. Calculations of pre-mining APRs can be found within 0VIX’s documentation.

Users will be able to claim their mined $VIX after the token launch, which will be subject to vesting terms yet to be defined.

veTokenomics

As I previously mentioned, 0VIX will be the first lending market to implement a veToken model (ve stands for “vote escrow”) once their token is released. In this model, users lock their tokens (VIX in this case), forfeiting them to the protocol for a period of time in return for veTokens (veVIX) that give voting decisions and increased rewards to the holders. veVIX holders will vote to decide on which markets receive VIX emission flows, getting a direct say in how rewards are distributed.

Market Research

As my relatives often like to remind me (now more than ever), crypto markets are very volatile. Extreme volatility puts strain on lending markets in particular, as the value of user collateral can dramatically decrease in a short period of time. When you combine this volatility with high asset correlation, an overall lack of liquidity and the reckless use of leverage, it becomes clear how difficult a balancing act maintaining a DeFi lending platform really is.

0VIX has done a considerable amount of market research, stress testing and risk assessment in order to prepare the protocol for extreme market events. They’ve tested multiple parameters through a great number of protocol simulations using highly volatile price trajectories for multiple assets, all with the goal of building market resilience and ensuring protocol safety and security.

You can read through their entire report with the link provided above; or check out their article released on the subject for a more digestible version.

Audits

0VIX has received audits from three separate firms: Watchpug, PeckShield and Omniscia. The reports from each are listed below:

Thanks for reading, be sure to keep an eye on the Blockbytes website for more project overviews and much more!